MDURATION(SettlementDate, MaturityDate, Coupon, Yield, Frequency, Basis)

- Where is the security's settlement date (a date when coupon or a bond is purchased),

- is the security's maturity date (a date when coupon or a bond expires),

- is the security's annual coupon rate,

- is the security's annual yield,

- is the number of coupon payments per year, and

- is the type of day count basis to use.

MDURATION() gives the modified Macauley duration of a security for an assumed par value of $100.

Description

MDURATION(SettlementDate, MaturityDate, Coupon, Yield, Frequency, Basis)

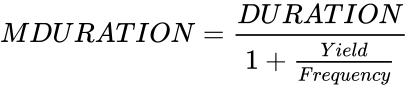

- MDURATION() or modified duration calculates the percentage derivative of price with respect to yield.

- Formula-

- and dates should be entered either in 'date format' or 'dates returned using formulas'. If dates are not valid, Calci displays #N/A error message.

- If date ≥ date, Calci displays #N/A error message.

- and values must be greater than or equal to zero.

- The values for should be 1,2 or 4.

For Annual payment, frequency = 1,

For Semi-annual payment, frequency = 2,

For Quarterly payment, frequency = 4.

- value is optional. If omitted, Calci assumes it to be 0.

Below table shows the use of values:

| Basis | Description |

|---|---|

| 0 | US (NASD) 30/360 |

| 1 | Actual/actual |

| 2 | Actual/360 |

| 3 | Actual/365 |

| 4 | European 30/360 |

- If value is other than 0 to 4, Calci displays #N/A error message.

Examples

Consider the following example that shows the use of MDURATION function:

| September 10, 2010 | ||

| September 10, 2014 | ||

| 6% | ||

| 9.0% | ||

| 2 | ||

| 1 |

=MDURATION(A1,A2,A3,A4,A5,A6) displays 3.8035273385670787 as a result. =MDURATION(DATE(2013,6,1),DATE(2013,12,31),"8%","9%",1,1) displays 0.9174311926605504 as a result.