Difference between revisions of "Manuals/calci/BETADIST"

Jump to navigation

Jump to search

| Line 14: | Line 14: | ||

*Normally <math>x</math> lies between the limit <math>a</math> and <math>b</math>, suppose when we are omitting <math>a</math> and <math>b</math> value, by default <math>x</math> value with in 0 and 1. | *Normally <math>x</math> lies between the limit <math>a</math> and <math>b</math>, suppose when we are omitting <math>a</math> and <math>b</math> value, by default <math>x</math> value with in 0 and 1. | ||

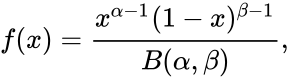

*The Probability Density Function of the beta distribution is: | *The Probability Density Function of the beta distribution is: | ||

| − | <math>f(x)=\frac{x^{\alpha-1}(1-x)^{ \beta-1}}{B(\alpha,\beta)},</math> where <math>0 | + | <math>f(x)=\frac{x^{\alpha-1}(1-x)^{ \beta-1}}{B(\alpha,\beta)},</math> where <math>0 \le x \le 1</math>; <math>\alpha,\beta >0 </math> and <math>B(\alpha,\beta)</math> is the Beta function. |

*The formula for the Cumulative Beta Distribution is called the Incomplete Beta function ratio and it is denoted by <math>Ix</math> and is defined as : | *The formula for the Cumulative Beta Distribution is called the Incomplete Beta function ratio and it is denoted by <math>Ix</math> and is defined as : | ||

| − | <math>F(x)=Ix(\alpha,\beta)=\int_{0}^{x}{t^{α−1}(1−t)^{\beta−1}dt} {B(p,q)}</math>, where <math>0 \le x \le 1</math>0 ; <math>\alpha,\beta>0</math> | + | <math>F(x)=Ix(\alpha,\beta)=\int_{0}^{x}\frac{t^{α−1}(1−t)^{\beta−1}dt} {B(p,q)}</math>, where <math>0 \le x \le 1</math>0 ; <math>\alpha,\beta>0</math> and <math>B(\alpha,\beta)</math> is the Beta function. |

*This function will give the result as error when | *This function will give the result as error when | ||

1.Any one of the arguments are non-numeric | 1.Any one of the arguments are non-numeric | ||

2.<math>\alpha \le 0</math> or <math>\beta \le 0</math> | 2.<math>\alpha \le 0</math> or <math>\beta \le 0</math> | ||

3.<math>x<a</math> ,<math>x>b</math>, or <math>a=b</math> | 3.<math>x<a</math> ,<math>x>b</math>, or <math>a=b</math> | ||

| − | 4.we are not mentioning the limit values <math>a</math> and <math>b</math>, by default it will consider the Standard Cumulative Beta Distribution, <math>a = 0</math> and <math>b = 1</math>. | + | 4.we are not mentioning the limit values <math>a</math> and <math>b</math>, |

| + | by default it will consider the Standard Cumulative Beta Distribution, <math>a = 0</math> and <math>b = 1</math>. | ||

==Examples== | ==Examples== | ||

Revision as of 05:39, 3 December 2013

BETADIST(x,alpha,beta,a,b)

- x is the value between a and b,

- alpha and beta are the value of the shape parameter

- a & b the lower and upper limit to the interval of x.

Description

- This function gives the Cumulative Beta Probability Density function.

- The beta distribution is a family of Continuous Probability Distributions defined on the interval [0, 1] parameterized by two positive shape parameters, denoted by and .

- The Beta Distribution is also known as the Beta Distribution of the first kind.

- In , is the value between and .

- alpha is the value of the shape parameter.

- beta is the value of the shape parameter

- and (optional) are the Lower and Upper limit to the interval of .

- Normally lies between the limit and , suppose when we are omitting and value, by default value with in 0 and 1.

- The Probability Density Function of the beta distribution is:

and

and  .

. ,

,  is the value between

is the value between  and

and  .

.where ; and is the Beta function.

where

where  ;

;  and

and  is the Beta function.

is the Beta function.

- The formula for the Cumulative Beta Distribution is called the Incomplete Beta function ratio and it is denoted by and is defined as :

and is defined as :

and is defined as :Failed to parse (syntax error): {\displaystyle F(x)=Ix(\alpha,\beta)=\int_{0}^{x}\frac{t^{α−1}(1−t)^{\beta−1}dt} {B(p,q)}} , where 0 ; and is the Beta function.

- This function will give the result as error when

1.Any one of the arguments are non-numeric 2. or 3. ,, or 4.we are not mentioning the limit values and , by default it will consider the Standard Cumulative Beta Distribution, and .

or

or  3.

3. ,

, , or

, or  4.we are not mentioning the limit values

4.we are not mentioning the limit values  and

and  .

.

Examples

- BETADIST(0.4,8,10) = 0.359492343

- BETADIST(3,5,9,2,6) = 0.20603810250

- BETADIST(9,4,2,8,11) = 0.04526748971

- BETADIST(5,-1,-2,4,7) = NAN

See Also